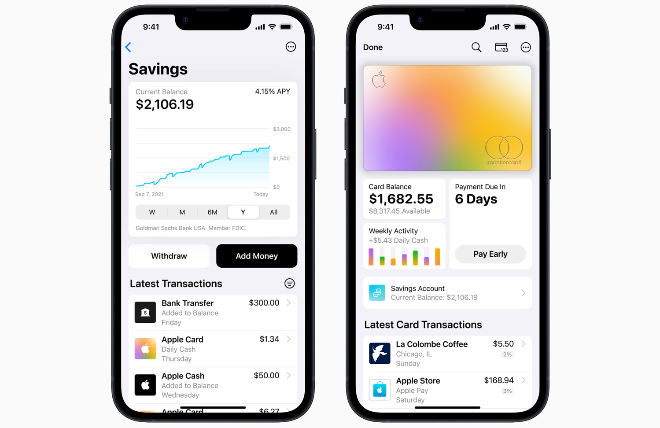

Apple has considerably more global reach and consumer trust than most banks. Is it any wonder, then, that it is slowly but surely turning into a financial institution? Even before it co-launched, with Goldman Sachs, a market-leading savings account that pays 415 times the lowest rate at old line institutions such as Chase or Bank of America, it already had its own credit card, peer-to-peer lending capacity, Wallet app and a “buy now, pay later” service that allows customers using their digital wallets to pay off their purchases — interest free — in installments.

Apple does appear well placed to solve some of the problems that have plagued traditional banking for years. Take the BNPL programme, for example. The company actually funds the loans largely from its own balance sheet, which had a hefty $165bn in cash and marketable securities as of the first quarter of 2023, with total debt of $111bn. This ratio sits in contrast with most banks, which do their daily business with 90 per cent or more borrowed money.

Should Apple hasten the exodus of deposits from the traditional banking sector in ways that start to undermine already beleaguered financial institutions, I suspect that regulators will take a closer look at the business model. The company will also have to be careful to avoid compromising consumer data in ways that trigger antitrust issues.

But until then, I suspect we will see more banking done via iPhone.