The new BNPL offering carries zero fees and interest, provided that someone pays back their loan on time. If they don’t, they’ll be disqualified from the scheme. And in all likelihood many will indeed miss a payment: Data shows one in 10 U.S. consumers who take out BNPL loans—often through companies like Affirm and Klarna—are ultimately hit with late fees.

“It’s an aggressive and smart move by Apple to double down its efforts on this category,” says Dan Ives, managing director and senior equity analyst at Wedbush Securities. “This is a shot across the bow at Affirm and other competitors.”

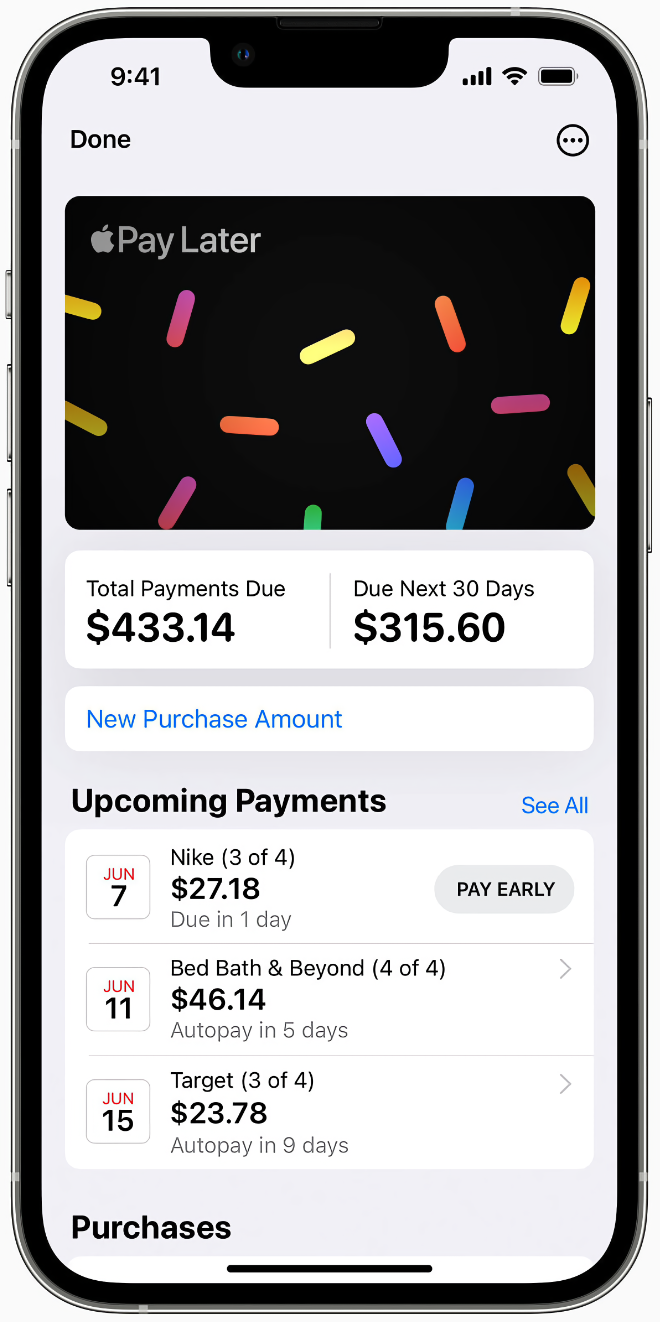

While Apple will have plenty of competition in the marketplace, they’re in a good position to succeed, according to Benedict Guttman-Kenney, an economist at the University of Chicago Booth School of Business. “If you look at Apple, they’ve already got a large payments infrastructure,” he says. “They’ve already got a large client base. They’re in a very good position to compete with the existing lenders.”

But the entry into the BNPL space also has wider ramifications beyond who’s winning and who’s losing in the fintech world. By making BNPL more mainstream, Apple could push more people into debt…

If there’s one thing Apple’s entry into the sector could trigger, it’s more scrutiny by the Consumer Financial Protection Bureau (CFPB), the federal government watchdog. Last year the CFPB raised concerns over BNPL lenders’ use of customer data to target those same people with advertising and lead generation.